A nation’s industrial policy significantly influences its innovation capabilities, industrial competitiveness, and the well-being of its citizens. The Future Made in Australia Act (FMiA) is an industrial policy that aims to tackle grand challenges the country is facing, such as climate change, technological sovereignty, and sustainable productivity.

This policy signifies a shift from a neoliberal to a more mission-driven approach in policymaking, reflecting the concern to transform the country from a resource and commodity-based economy to one that is driven by innovation and focused on adding more value in sustainable ways in a rapidly changing technological and geopolitical landscape.

This shift encompasses protectionist measures but also proactive investments in sectors with high potential, including building local manufacturing capabilities for a green energy transition, attempting to ensure that Australian industries regain competitiveness on the global stage.

By aligning industrial policy with broader economic goals, such as sustainability and technological innovation, Australian policymakers argue that this approach enables the country to harness future growth opportunities.

However, this policy shift has been criticised because its efficacy cannot be guaranteed. A fundamental concern with the mission-driven approach is the unpredictability of emerging industries and the speed of technological development. Additionally, rapidly changing geopolitics can influence the demand and supply balance in global supply chains, potentially rendering investments in targeted industrial sectors wasteful.

To avoid the pitfalls of mission-driven industrial policy and to ensure that Australia’s industrial policies are targeting the right sectors in their mission-oriented pursuit, Australia should adopt multifaceted policy programs, taking into consideration both vertical and horizontal policy programs.

These programs should focus on developing strategies which engage with established and emerging technologies and firms, building strengths in both curiosity-driven research and firm capabilities, fostering global and local partnerships, and cultivating an ecosystem mindset that combines all these elements.

This requires Australia to diversify its technology partnerships and supply chains, and advocate for open, interoperable technology standards for global use. Effective programs should also foster a business environment that benefits a broad spectrum of Australians, not just a few established industries and firms. These programs will transcend merely joining a global subsidies arms race by pursuing a ‘moonshot’ strategy.

Emerging industrial interventionism

Industrial policy broadly refers to any policy that affects a country’s industrial development or competitiveness.

Such policies play an instrumental role in latecomer countries, such as China. They are crucial to China’s industrial development, not just because of the large state presence in its economy, but also due to the imbalances between sectors and regions, and between state-owned and private businesses.

In such countries, industrial policies aim not only to compensate for market failures but also to actively intervene in economic structural reforms, increase industrial competitiveness, and support strategic socio-technical transitions.

In developed countries, traditionally associated with protectionism and state intervention, industrial policies are only deemed effective when they focus on market or systems failures as a complementary force to market mechanisms. However, past policies focused solely on market mechanisms have proven less effective in delivering more equitable wealth distribution, sustainability, and quality jobs, especially when facing emerging industrial powers such as China.

Against this backdrop, mission-driven policies are increasingly seen as tools to counter China’s state-backed capitalism and retain and enhance national competitiveness. Furthermore, the US-China tech war has heightened the focus on industrial policy measures, as both countries strive to protect and advance their technological capabilities.

This is particularly relevant in the post-pandemic era, where global supply chain disruptions have underscored the vulnerabilities of over-reliance on foreign suppliers, spurring efforts to re-shore manufacturing capabilities.

This conflict has led to increased tariffs, export controls, and investment restrictions aimed at safeguarding domestic industries and national security. Both the US and China have bolstered their tech sectors with subsidies, research funding, and intellectual property protections.

The tech race’s ripple effects have prompted other nations to adopt similar industrial policies, adapting to the shifting global tech landscape and mitigating risks from the US-China rivalry. As a result, we have witnessed in the developed world a resurgence of market-shaping policies focused on innovation and transformation.

These policies, targeted at strategic sectors such as semiconductors, electric vehicles, renewable energy, and critical minerals, are missions led by the US to counter China’s growing influence. Examples include the US CHIPS Act, the US Inflation Reduction Act (IRA) and the European Commission’s Critical Raw Materials Act (CRMA), which all exemplify these efforts.

Australia, too, has seen a resurgence of interventionism in its industrial policies, reflecting a strategic shift in government policymaking. This trend is exemplified by initiatives such as the Future Made in Australia Act (FMiA) and various targeted government funds, particularly in sectors such as critical minerals supply chains, which are essential for energy security and green technologies.

Does this shift in policymaking, especially joining the subsidies arms race, truly represents the best interest of Australia – and if so, for which groups? Additionally, what measures and mechanisms can be implemented to ensure that, if there are benefits from this shift, they can reach everyone in the country?

Funding a Future Made in Australia

The 2024-2025 Budget has allocated substantial funds to support sectors deemed critical to Australia by the FMiA. Treasurer Jim Chalmers stated that the $22.7 billion FMiA package ‘will help make us an indispensable part of the global economy.’

This includes, for example, transforming Australia’s battery industry by assisting manufacturers in moving up the battery value chain through the new Battery Breakthrough Initiative ($523.2 million over seven years); and supporting Australian critical minerals processing through the new Critical Minerals Production Tax Incentive ($7 billion over 11 years starting from 2023-24).

These incentives will provide refundable tax rebates for the eligible costs involved in enhancing manufacturing or processing capabilities in Australia, aiming to prevent and mitigate foreign interference.

Various stakeholders have responded positively to this policy, emphasising its potential benefits for the climate, workers, and firms in relevant sectors. There are, however, valid concerns about its efficacy and the potential for unintended consequences. Government planners may not have sufficient control to ensure the long-term success of industrial policies for several reasons.

First, major subsidy programs, tax credits, procurement preferences, and other incentives are being deployed to subsidise qualified companies willing to re-shore their manufacturing capabilities, as seen in the US CHIPS Act and the IRA. Such policies risk exacerbating wealth inequality if not crafted and executed carefully.

These policies often channel subsidies and incentives toward large corporations with established technologies and manufacturing bases, and effective lobbying power, consolidating their market dominance. A prime example is Intel’s disproportionate benefit from the US CHIPS Act, potentially at the expense of smaller, innovative firms.

In Australia, notable regional disparities in household income and net wealth exist, with mineral-rich states significantly outperforming those that are not, largely due to the robustness of the mining sector. If subsidies are provided to enhance Australia’s critical minerals processing and manufacturing capabilities, they will predominantly benefit firms located near mining sites, in mineral-rich states. Thus, regional disparities are likely to widen rather than be reduced through these policy interventions.

Second, designing and implementing effective industrial policies that avoid past pitfalls requires robust institutional frameworks, monitoring mechanisms, and political insulation. In addition, the success of industrial policies hinges on navigating complex dynamics of political economy, interest group pressures, and ensuring policies are driven by sound technocratic criteria rather than rent-seeking motives.

For example, unilateral industrial policies could exacerbate trade frictions and spark retaliatory moves, undermining their intended benefits. Such policies require highly skilled, well-informed, risk-aware, and decisive policymakers, and such people tend to be few and far between internationally.

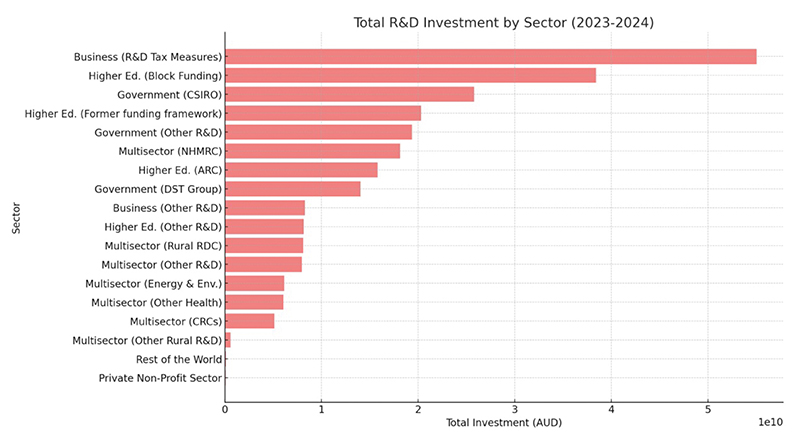

Third, lessons from historical budgets for R&D and innovation can also shed light on challenges faced in future industrial policies. A detailed analysis of Australia’s Science, Research, and Innovation (SRI) budget (2023-2024) reveals that the top two sectors benefiting most from government subsidies in R&D and innovation are business, through R&D tax measures, and higher education though block funding. The distribution of the SRI budget is shown in the chart above, which was generated using data from the SRI budget table 2023-24.

Around 60 per cent of R&D tax incentives for businesses, approximately $16.9 billion, went to large businesses, while 40 per cent, approximately $11.27 billion, went to small and medium-sized enterprises (SMEs). This budget allocation may reflect the relative contributions of these two groups to the country’s GDP.

In 2022, SMEs contributed one-third of the GDP, although they accounted for 98 per cent of all enterprises in Australia, employed two-thirds of the workforce, and provided training for nearly half of all apprentices and trainees.

Targeted sectors identified in the FMiA, particularly programs to enhance value-added capabilities in critical minerals processing and battery manufacturing, suggest that perhaps more subsidies will be channeled towards the mining sector, primarily benefiting large mining and manufacturing companies that have the established capabilities to engage in such activities.

The potential for SMEs to develop value-added manufacturing or refining capabilities with the help of subsidies is constrained by their lack of economies of scale, which may limit their ability to benefit from such policies.

SRI budget analysis also suggests that over 63 per cent of the funding went to science and research, including basic research, applied technology development, and advanced research initiatives. The remainder went to investment in innovation, including technology commercialisation, entrepreneurial support programs, startup accelerators, and new venture support.

Again, this budget allocation has likely benefited large businesses as they have more extensive R&D activities, and the capacity to absorb R&D knowledge from external sources. SMEs may benefit more from investment in innovation, rather than R&D support.

The fragmented nature of research and innovation program funding in Australia, evidenced by 160 budget line items spread across 14 portfolios, underscores a critical structural issue that can impede the efficiency and effectiveness of national development initiatives.

This fragmentation can lead to inefficiencies such as duplicated efforts, misallocated resources, and lack of strategic alignment across different sectors and disciplines, all of which are particularly detrimental for a medium-sized economy like Australia.

SMEs are crucial for fostering a diverse and dynamic economy. They are often recognised for their ability to innovate and adapt quickly to changing market and technological conditions. More innovation-driven industrial policy programs that nurture entrepreneurship and innovation are essential.

Vertical vs horizontal industry policies

Vertical policy programs

Sector-focused industrial policies represent vertical strategies that target specific sectors or activities, aiming to shape industries deemed strategic and critical to a country’s development.

A downside of such an approach is that it can prevent firms from exploring and thriving in areas that receive less government support. Therefore, sector selection is crucial in vertical policymaking, requiring clear rationales and performance measures to ensure the correct policy directions and effective resource allocation.

Industrial policy decisions are rarely straightforward, influenced by a mix of political and economic cycles, sector-specific dynamics, lobbying capacities, and increasingly geopolitical considerations. Policymakers must foster innovation and address systemic challenges, considering their unique positions in the global technology value chain.

We now turn to Australia’s unique positions in two sectors: critical minerals and AI and outline the potential risks in sector-focused policymaking.

Australia is well endowed with critical minerals such as lithium, rare earths, and cobalt, making it a leading global producer of several of these commodities. While well-positioned due to its abundant resources, it faces significant risks from supply chain interdependencies amid geopolitical tensions.

As one of the few suppliers in the US-led Minerals Security Partnership, Australia has forged strategic alliances with allied nations to secure reliable supply chains for critical minerals, serving as a counterbalance to China’s dominance. However, the US IRA mandates that Australian miners limit Chinese equity stakes to below 25 per cent to qualify for subsidies. This requirement necessitates a reassessment of ties with China and could invite retaliation from Chinese downstream manufacturers.

Australia’s domestic capabilities for downstream processing and manufacturing of critical minerals remain underdeveloped. Its critical minerals sector is heavily intertwined with China, which dominates minerals processing and manufacturing. A large proportion of Australia’s mineral exports is destined for China, making the sector highly susceptible to trade disruptions and geopolitical tensions.

Establishing these capabilities would require substantial investments, technological innovation, and environmentally sustainable solutions. Additionally, Australia’s high labour costs make domestically produced minerals less competitive in the global market.

On the other hand, countries rich in resources such as Chile, Argentina, and Indonesia are also vying to ascend the critical minerals value chain by attracting investment and technology transfer, often through partnerships with China. They are competitors to Australia in critical minerals.

Moving up the global value chain of critical minerals production, as advocated by the FMiA, may lead Australia to a position where it can only export these minerals to America and other partner nations when supplies from China are disrupted. If that occurs, Australia might be confined to a niche role and miss opportunities in other industries.

In the AI sector, despite its significant potential to transform industries and drive productivity growth, Australian industrial policy targeting AI is limited, particularly in funding AI research and innovation in the business sector. This oversight represents a missed opportunity to harness the transformative power of AI.

AI is not merely a standalone sector but thrives within an ecosystem of data, computational resources, and talent. Despite Australia’s notable advances in AI research, it faces significant constraints that hamper its ability to fully realize the value of AI research.

The availability of data and computational resources is a critical limitation. Advanced AI research necessitates vast datasets and substantial computational power. While Australia has robust digital infrastructure, it falls short of the immense scale seen in AI giants such as the U.S. and China. Additionally, the ecosystem for AI talent in Australia, though growing, lacks the funding for the sustained innovation and entrepreneurship required for AI development.

In 2023, the US private sector invested $62.7 billion in AI, accounting for 73 per cent of global AI investment. Australia’s private sector investment in AI is modest. Over-reliance on public funding, especially in research institutions, limits the agility and scalability of AI initiatives, stymieing growth in the country.

Job availability and mobility are paramount in fostering a dynamic AI ecosystem. The AI industry is characterised by high personnel mobility, requiring a fluid exchange of skills and talent between private enterprises, academia, and research institutions. Private sector involvement in creating AI jobs is crucial. In the US and China, private enterprises dominate AI job creation.

In Australia, the job market for AI-related positions in industry is limited, leading many talented people to seek opportunities in more developed markets. Australia must develop a national AI strategy that outlines clear goals, priorities, and investment plans for AI research, development, and adoption across industries.

Targeted funding and incentives for businesses, especially SMEs, to invest in AI technologies and AI-driven solutions are critical for enhancing productivity, innovation, and industrial competitiveness. The government also needs to actively participate in the international standardisation of an AI governance framework that balances data sharing and utilisation with privacy, security, and ethical considerations.

Horizontal policy programs

To address these constraints and implement policy programs that leverage Australia’s unique strengths to develop an irreplaceable position in the global technology value chain, policymakers need also to adopt horizontal policy programs.

Horizontal policies aim to enhance the overall business environment, benefiting a wide range of sectors and many economic actors in the country. These include improving infrastructure, providing access to diverse finance, promoting entrepreneurship-driven R&D and innovation, enhancing education and skills training, enabling talent mobility, and streamlining regulations.

Such measures create a conducive ecosystem for entrepreneurship and innovation without favouring specific industrial sectors or firms.

Building common-user infrastructure, such as utilities, transport, and processing hubs and facilities, can attract inventors, entrepreneurs, and small businesses to invest in these sectors, by mitigating capital risks and facilitating the scaling of innovative technologies, not just to serve Australia’s but the global market.

For example, centralised processing hubs and common laboratory facilities can be instrumental for technologies in critical minerals. These hubs can provide shared access to mineral refining and manufacturing facilities, reducing costs and fostering innovation. Common laboratories equipped with analytical tools for testing new technologies and pilot plants for optimizing manufacturing processes can support startups and research institutions, driving innovation in a cost-effective manner.

To support AI research, Australia must invest in high-performance computing (HPC) centres and develop national data repositories, as shared-use computational resources and data infrastructure.

Establishing centralised data hubs will also facilitate data sharing and collaboration among researchers, enhancing the overall research environment. These resources will provide the necessary computational power and data access for cutting-edge AI development.

Alongside merely scaling up manufacturing, where Australia doesn’t enjoy advantages due to its small and comparatively expensive workforce, the country should focus on enabling technologies that leverage its strengths in high-tech services.

By focusing on specialised products that require complex technologies and skilled labor, Australia can avoid direct competition with economies that benefit from lower labor costs. Switzerland, for example, excels in areas like pharmaceuticals, precision machinery, and high-tech instrumentation, where quality, reliability, and technological superiority are more critical than cost.

These enabling technologies include automated production lines for manufacturing, advanced materials and sensors, innovative equipment and tools, and recycling technologies. High labour costs can be offset by increased investment in automation technologies, which reduce the need for manual labor and increase production efficiency.

Advanced robotics and AI can lead to significant productivity gains in manufacturing processes. While details of the newly announced national robotics strategy are limited, it suggests that the government intends to unveil specific strategies and initiatives aimed at developing and adopting robotics technologies.

Place-based innovation ecosystems are designed to leverage local strengths to boost economic growth and technological innovation. These ecosystems function by connecting research institutions, startups, established companies, and government bodies within a geographical area, focusing on specific technological or industrial verticals. The dual nature of these ecosystems, both vertical and horizontal, allows for a tailored approach that addresses specific industry needs while fostering a general environment conducive to innovation.

This approach, exemplified by models such as Germany’s Fraunhofer Institutes, the UK and Norwegian Catapults, the US ManufacturingUSA Institutes, and the NSF Regional R&D Engines, offers a compelling blueprint for Australia as it seeks to recalibrate its industrial strategy.

Australia’s vast geography and the economic diversity of its regions mean that one-size-fits-all approaches are less likely to succeed. Ensuring that all stakeholders, including governments at all levels, industry, academia, and the community, are aligned in their goals and cooperative in their efforts, is key.

Australia needs to develop funding models that ensure sustainability without excessive reliance on government funding. Public-private partnerships can leverage government funds to boost private sector contributions, ensuring a balanced investment landscape.

For example, promoting venture capital investment through sector-specific funds supported by government incentives can attract private investment. Engaging in international technological initiatives and seeking funding from global consortia can provide additional resources and collaborative opportunities.

In Australia, a vibrant talent ecosystem is also crucial. This can be achieved by incentivising technology job creation in the private sector through tax incentives and grants for R&D and innovation employment as well as performance, further encouraging industry-academia collaborations, and better supporting startups and SMEs through improving risk tolerance.

It has long been appreciated how programs that connect startups with universities and research institutions foster innovation and ensure the continuous flow of talent, and these need to be accentuated.

Conclusion

So, does Australia’s mission-driven industrial policy truly represent the best interests of the country, and can the benefits be shared across various regions and firms? Yes and no.

Facing increasing geopolitical uncertainty, Australia must pursue an independent industrial policy to strengthen its global competitiveness and resilience. However, a mix of vertical and horizontal policy programs is needed to ensure that such policies target the right “moonshots” and the benefits are available to many Australian firms and individuals.

The pressure is on government to build on Australia’s strengths without being captured by the interests of the strongest at the expense of the emergent. This requires exceptional policymaking and implementing capabilities. Furthermore, Australia’s response to adverse international pressures will paradoxically require greater internationalisation.

Providing Australia can contribute distinctive advantages, collaborate with international research institutions and participate in global technology forums, the risks associated with techno-nationalism can be mitigated. These partnerships will provide access to global knowledge pools, foster international collaboration, and ensure that Australia remains competitive in the rapidly evolving technological and geopolitical landscape.

This article is part of The Industry Papers publication by InnovationAus.com. You can order your hard copy of The Industry Papers here.

36 Papers, 48 Authors, 65,000 words, 72 page tabloid newspaper + 32 page insert magazine

The Industry Papers is a big undertaking and would not be possible without the assistance of our valued sponsors. InnovationAus.com would like to thank Geoscape Australia, The University of Sydney Faculty of Science, the Semiconductor Sector Service Bureau (S3B), AirTrunk, InnoFocus, ANDHealth, QIMR Berghofer, Advance Queensland and the Queensland Government.

Associate Professor Dr Marina Yue Zhang, Associate Professor at the Australia-China Relations Institute at the University of Technology Sydney (UTS: ACRI). She previously held positions at the University of New South Wales (UNSW) and Tsinghua University. Marina holds a bachelor’s degree in biological sciences from China’s Peking University, and an MBA and a PhD in innovation studies from the Australian National University. She is the author of three books, including Demystifying China’s Innovation Machine: Chaotic Order, co-authored with Mark Dodgson and David Gann.

Professor Roy Green, Emeritus Professor and Special Innovation Advisor at the University of Technology Sydney (UTS). He is Chair of the Advanced Robotics for Manufacturing (ARM) Hub and the Port of Newcastle and has published widely in the areas of industry and innovation policy, including projects with the OECD and European Commission, and has led a number of government inquiries. Roy is on the Board of the CSIRO and the SmartSat CRC, is a member of the CSU Council and the newly established Australian Design Council. He was previously Dean of the UTS Business School.

Professor Mark Dodgson, Emeritus Professor at the University of Queensland; Executive-in-Residence at the University of Oxford; and Visiting Professor at Imperial College London. He has published 19 books and over 100 academic articles on innovation and entrepreneurship, and has researched and taught the subject in more than sixty countries. His current research is on the Oxford/AstraZeneca Covid-19 vaccine and the development of fusion energy.

Do you know more? Contact James Riley via Email.