Have you ever stopped to think about where all the digital services you use each day physically reside, or what powers them?

Whether you access them on your mobile, a tablet or a computer, those services are not really delivered atop fluffy clouds that float high above your head. Instead, they come to you care of radio signals received by antennae and routers that are connected to cables and ultimately track back to data centres.

The reality is that there’s a mountain of computing and communications infrastructure behind your every search, Uber Eats order, TikTok video, ChatGPT prompt, banking transaction, online purchase or social post.

Much of that infrastructure is in the data centres that power the cloud, making them essential to our ability to live, do business and innovate in the digital age.

Today’s data centres are home to email and file-sharing services such as Gmail, Dropbox, and Microsoft 365. They host the many business applications that reside in the cloud, from Canva for graphic design to Atlassian’s workflow solutions, SAP, and Xero for accounting and HubSpot and Zendesk for customer management and service support.

They underpin online government services and drive video tools like Cisco Webex and Zoom.

Because the businesses, governments, schools, hospitals, and other organisations we depend on are mostly powered by the cloud, data centres have become the engine rooms of our modern economy.

And those engines are revving even faster with the emergence of newer technologies including artificial intelligence (AI), the Internet of Things, 5G, quantum computing and virtual reality. This is, in turn, creating new challenges and opportunities.

Australia’s challenge is to build its cloud data centre capacity fast enough to realise the economic and social benefits offered by these breakthrough technologies – and to keep pace with all the other nations doing the same thing.

Our opportunity is to leverage this investment to simultaneously increase our supply of renewable energy and storage, thereby moving closer to meeting our national carbon reduction goals.

We need to more than double our data centre capacity in the next five years, according to market analysis, to meet the surge in demand being created by the newer technologies listed above.

This is a big ask for Australia and achieving it will require focused effort and new policies. But it also means it’s a big opportunity, given the billions of dollars being invested.

Our national data centre capacity has surged over the past five years, driven by cloud computing and the pandemic, which saw many of us shift to working remotely and becoming ever more reliant on digital services.

This growth has enabled businesses and governments to become more productive, lower their IT costs, increase their cybersecurity and resilience, and operate globally using global standards.

Analysis by Mandala suggests there are more than 200 data centres in Australia, including approximately ten that are large scale, excluding private on-premise data centres. High-tech cloud providers use these centres to deliver services to thousands of Australian businesses, schools, governments and not-for-profits.

Most of the largest data centres are in Sydney and run by hyperscale specialist data centre operators including AirTrunk, CDC Data Centres, Digital Realty, Equinix, Global Switch and NextDC. Some of the largest tech companies are now also building their own facilities.

Despite this we are a long way from meeting our data centre needs as we increase our use of digital services, embrace AI across all industries and generate more data, all of which requires greater computing power.

Analyst group IDC has estimated that consumers and businesses will generate twice as much data over the next five years as all the data created over the past decade. Globally, that will see the amount of data in data centres and digital devices grow from 10.1 zettabytes (ZB) in 2023 to 21ZB in 2027.

Meeting this demand means building more data centres and ensuring we have the power to run them. In fact, power is so essential to data centres that the industry measures capacity in terms of electricity supply rather than bits and bytes.

According to the Global Data Centre Index 2024, Australia’s data centres currently have a capacity of about 1.1 gigawatts (GW) and approximately 1.5GW of further third-party data centre capacity is under construction or soon to begin.

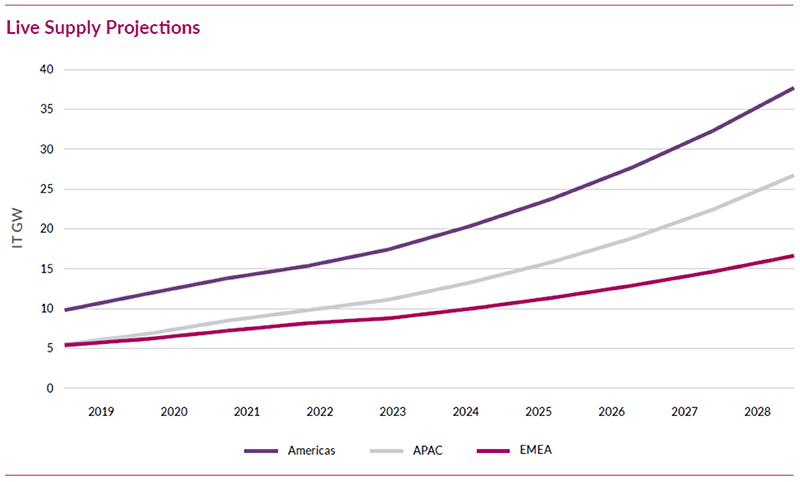

This rapid expansion is part of a global trend. As Figure 1 shows, Asia Pacific’s total data centre capacity was 5GW as recently as 2019. It is now around 12GW and expected to exceed 25GW by 2028.

Our region is growing at the fastest pace globally in line with the region’s fast-growing economies and rapid digital transformation.

This growth is raising concerns about energy availability and emissions from the related energy sources.

Some overseas governments have responded by restricting the creation of new data centres and the location of centres. Others have sought to apply management levers used in other industries, including power network load shedding.

Given the essential nature of data centres and their need for a constant, 24/7 energy supply, such policy responses can hurt both economies and societies.

We must therefore find ways to continue growing our data centre infrastructure without undermining our climate goals and ensuring energy reliability, which means expanding our clean energy generation and storage capacity and doing so in suitable locations.

It may seem counterintuitive that expanding data centres can play a key role in Australia’s energy transition, but they are a key ingredient. This is because data centre operators are keen to use low-carbon power sources and are prepared to invest in them.

As people in the tech industry know well, innovative ideas need business investment. They also know you need a strong market for your product to attract that investment. And that when industry invests with policy certainty and a strong market, prices come down meaning households pay less.

In Australia, our renewable sources of power generation are mainly wind, solar and pumped hydro.

These are supported by battery energy storage systems (BESS) and other solutions that enable the intermittent power from those sources to be used reliably in the power system.

Helping to bring online such firming resources is critical to data centre operators as our mission-critical services require not just clean energy but clean and stable energy supplies.

We need investment in both these areas as well as innovations that make data centres more energy efficient, such as liquid-to-chip cooling and changing configuration of the chips used, to meet the purpose using the right tools for the right job.

Australian Government authorities have approved 51 renewable energy projects in the past two years alone, which are expected to add 8.4 GW of clean energy to the national grid and help the nation prepare for the closure of coal-fired power stations.

That is almost three times the capacity of the country’s biggest coal-fired power stations and will be accompanied by storage systems to help deal with the intermittent supply challenge.

Data centre operators represent a ready-made customer base for such projects. Once in place, their requirements will be consistent, predictable, and long-term. This certainty can underpin a market that is essential to Australia’s energy transition and Net Zero ambitions.

Willing customers are lining up too. In addition to the pure-play data centre operators, AWS and Microsoft have announced plans to invest a substantial $18 billion in new data centre capacity in Australia from now to 2027. These investments are being matched by significant renewable energy supply deals.

Microsoft has signed a 15-year agreement to buy power from a new solar farm being built by Fotowatio Renewable Ventures Australia.

Google and AirTrunk have signed a similar agreement with OX2 that will enable the development of another solar farm that will add 25MW of new renewable energy generation to Australia’s power grid.

These arrangements will help ensure the solar projects are viable while enabling the technology firms to meet their own commitments to using 100 per cent renewable power in their data centres by 2030.

As Google Australia managing director Mel Silva said when announcing the investment, “Industry collaboration and innovation are crucial to achieving our ambitious sustainability objectives, including our efforts to drive a substantial increase in carbon-free energy capacity across the Asia Pacific region.”

Investments in power storage could also support the government’s Future Made in Australia policy to support local manufacturing.

BESS and other parts of the data centre supply chain are prime opportunities for local innovation and development, particularly because the industry is young and not weighed down by legacy issues.

AirTrunk, for example, is an Australian leader in developing water-to-chip cooling and there is an opportunity to build these innovations into the wave of new data centres rather than the challenges of retrofitting existing ones.

This would build on the history of data centres continually evolving and being a more efficient system than when servers were distributed in office buildings nationwide.

According to the International Energy Agency (IEA), the output of data centres rose by 340 per cent from 2015 to 2022, but the energy they used only increased by 20–70 per cent over the same period.

This has been an extraordinary achievement by the global data centre and tech industry, one that will need to be maintained and accelerated to support the next generation of technologies coming through.

Chief among these newcomers is generative AI, which uses more power than earlier approaches.

For example, the IEA reports that a traditional search query uses about 0.3-watt hours (Wh) of electricity, while processing a ChatGPT request consumes 2.9Wh. This will increase the energy needs of data centres in Australia and worldwide.

According to the IEA, data centres and transmission networks currently account for 1.0–1.5 per cent of electricity globally.

Looking ahead, Mandala analysis estimates that in Australia, data centre power demand will grow by 110 per cent from 2024 to 2030, provided power usage efficiency of data centres remains steady, as they support ever-smarter digital services.

Australia needs to recognise the scale of this change and plan accordingly to maintain and grow a globally competitive digital infrastructure in a sustainable fashion. In turn, good policy should be about recognising the opportunities for Australia to seize and becoming the leader in green data centres is there for the taking.

Australia has natural advantages and that position it well to be a renewables superpower.

The federal government has recognised this through the Capacity Investment scheme to encourage new investment in both renewable capacity and dispatchable capacity such as battery storage.

And while this focuses on the supply side, the data centre industry has much to offer as one of the largest industrial sectors to underwrite and offtake (purchasing of energy) on the demand side.

Because the government’s Future Made in Australia (FMiA) policy is also about making Australia a renewable energy superpower through its focus on supply chains, the data centre industry can play a role.

Three of the five industries identified in the policy could play a role in the data centre supply chain including green metals, renewable hydrogen, and solar and battery storage – highlighting the sector’s key position to drive real change. Why not add green data centres and sustainable AI as another key pillar of FMiA?

The tech industry also has the potential to accelerate and contribute to underwriting key projects in the transformation of the power grid.

Large projects are underway to connect massive renewable energy zones, grid-scale energy storage projects and to increase grid interconnection across the eastern states, changing the shape of the transmission network.

Digital services in cloud and AI are similarly reliant on this timely transmission augmentation. This means there are opportunities for the industry to engage more closely with grid companies , for the benefit of the wider transition.

Government can play a role by using underutilised policy levers – facilitating and connecting. Increasing communication and coordination between government, data centre operators, the energy industry and telecommunications companies will help find novel solutions.

The growth of digital services and now AI requires a new conversation and a much greater level of collaboration across the industry value chain.

An important role of government is to prepare for the future and often looking to the past provides a lesson.

With the National Broadband Network, we proactively rolled out a national fibre network to complement mobile and create a robust digital infrastructure. Yet we did so based on only a vague idea of the future.

We didn’t know exactly what people would do with broadband and other digital infrastructure, but we could see they were a good idea and committed to building them as quickly as possible.

Today, we can see how AI, quantum computing and other innovations will solve major problems and transform our economy and society. We also know we need to move to a new energy paradigm. The question is, are we are matching our digital economy ambitions with our energy transition goals to deliver the best outcomes for Australia?

Belinda Dennett, head of government relations, AirTrunk. Belinda has 20 years’ experience in tech policy, both in government and the private sector. She was a senior advisor on the digital economy in the Rudd and Gillard Governments before moving into the private sector leading Microsoft’s corporate affairs team in Australia, and more recently joining AirTrunk to establish its government relations and public policy function. She has qualifications in law and business.

This article is part of The Industry Papers publication by InnovationAus.com. Order your hard copy here. 36 Papers, 48 Authors, 65,000 words, 72 page tabloid newspaper + 32 page insert magazine.

InnovationAus.com would like to thank our sponsors Geoscape Australia, The University of Sydney Faculty of Science, the Semiconductor Sector Service Bureau (S3B), AirTrunk, InnoFocus, ANDHealth, QIMR Berghofer, Advance Queensland and the Queensland Government.

Do you know more? Contact James Riley via Email.